The Influence of Financial Strain on Choices in Personal Injury Settlements shapes how injured people weigh bills, risk, and long-term recovery after an accident.

In brief

- Financial strain often pushes injured people toward fast offers before the full cost of care is known.

- Personal injury settlements often cover more than current medical bills, including lost income, future treatment, and reduced earning power.

- Financial stress affects judgment during settlement negotiations, especially when rent, food, and transportation costs keep rising.

- Legal decisions made too early often weaken a claim if evidence is still missing or injuries are still developing.

- Claimants often have other short-term options, including payment plans, lien-based treatment, and legal guidance before signing a release.

Why Financial Strain Changes Personal Injury Settlements Fast

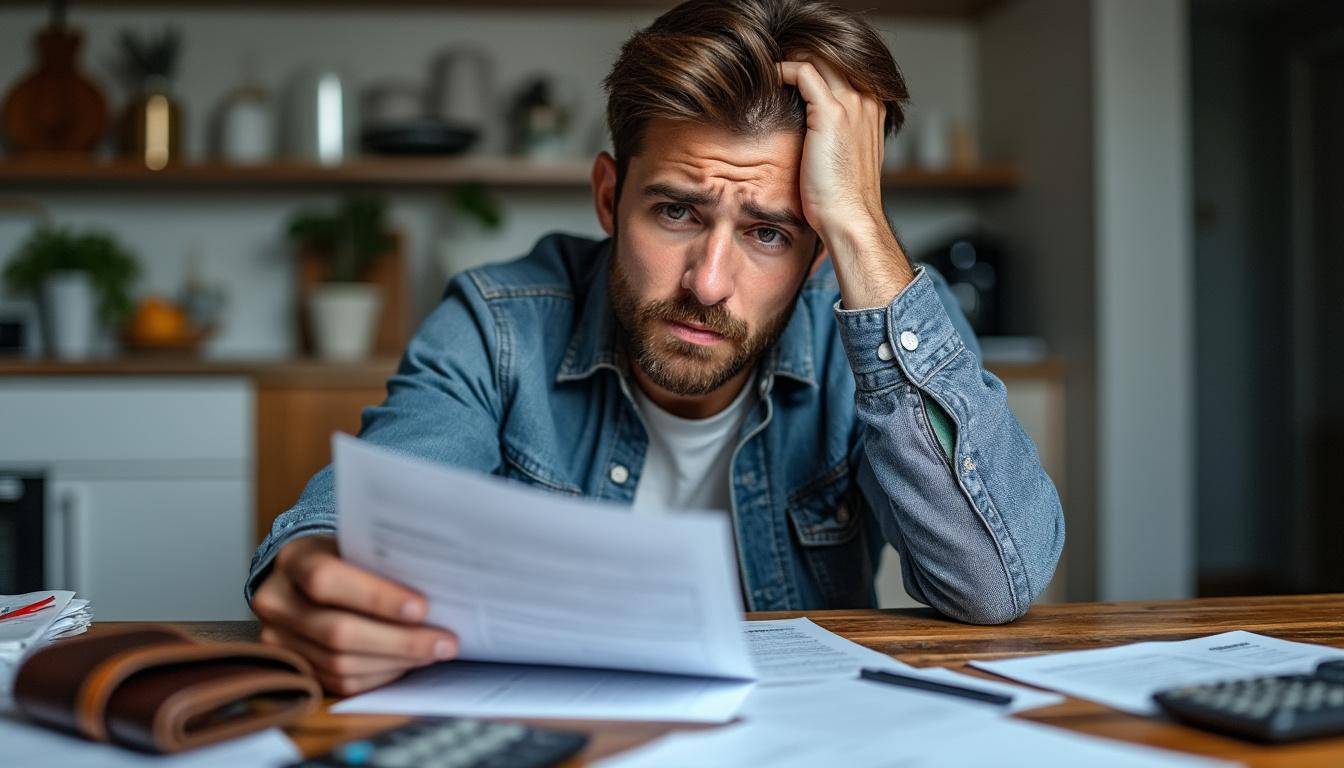

On a Tuesday morning, the crash is over, but the bills keep coming. Rent is due. The pharmacy needs payment. A follow-up scan is scheduled. Work hours are gone, and the phone rings with an insurance offer that sounds like relief. The Influence of Financial Strain on Choices in Personal Injury Settlements starts right there, in the gap between what hurts now and what the injury will cost later.

The Influence of Financial Strain on Choices in Personal Injury Settlements is not a theory. It plays out in homes where groceries cost more each week and missed paychecks turn small debts into urgent problems. Financial strain changes how people measure risk. A lower offer today may feel safer than waiting months for a fuller result, even when the injury picture is incomplete.

That tension matters in personal injury law because early numbers often arrive before the evidence does. Doctors may still be tracking nerve damage, therapy needs, or whether surgery will follow. Yet insurers often move early because early closure limits their exposure. The Influence of Financial Strain on Choices in Personal Injury Settlements becomes strongest when the injured person needs money before the medical story is finished.

Many claimants do not realize how final a signed release becomes. In most cases, once a settlement is accepted, the claim ends. If symptoms worsen later, if another procedure becomes necessary, or if a return to work fails, the cost often falls on the injured person. The Influence of Financial Strain on Choices in Personal Injury Settlements is severe because a short-term cash need can reshape a long-term legal outcome.

Courts do not value a case based on stress alone. They look at proof. Medical records, wage loss documents, witness statements, crash data, surveillance footage, employer logs, and digital records all matter. Strong claims often take time to build because evidence rules matter, and rushed files often leave value on the table. The Influence of Financial Strain on Choices in Personal Injury Settlements is often strongest at the worst possible moment, before the file is ready.

If you have been hurt in a car crash, workplace event, or fall, your rights deserve a calm review before money pressure decides the case for you. A useful first step is understanding timing and documentation in claims such as filing timelines and building a robust case. Another is learning why expert representation matters when insurers push for speed. The core lesson is simple. The Influence of Financial Strain on Choices in Personal Injury Settlements often turns urgent need into costly legal decisions.

Personal Injury Settlements Often Miss Future Costs When Financial Stress Takes Over

The Influence of Financial Strain on Choices in Personal Injury Settlements becomes clearer when you break down what a fair claim is supposed to include. A settlement is not only about the emergency room invoice. It often includes current treatment, future care, lost wages, reduced earning capacity, pain, emotional distress, and out-of-pocket costs tied to daily life after the injury. Under economic pressure, many people focus on the bill due Friday, not the therapy still needed three months from now.

Take a common example. A delivery driver suffers a back injury in a collision. At first, doctors expect a strain. Weeks later, the pain radiates, lifting becomes difficult, and imaging shows disc damage. If the driver accepted a quick payment in week two, the later treatment, work limits, and lower income may never be reflected in the final compensation. The Influence of Financial Strain on Choices in Personal Injury Settlements often lies in what is still unknown when the first offer arrives.

Insurance carriers understand this timeline. Early offers are often made before the diagnosis settles, before specialists weigh in, and before the injured person knows whether recovery will be full. That is why settlement negotiations demand patience, records, and a realistic forecast. Pressure changes the mental math. Certainty now feels better than a stronger outcome later, even when the later path would better reflect the injury.

There is another problem. Rushed cases often miss evidence beyond medical receipts. A strong personal injury case may involve witness statements, electronic data from a vehicle, business records, maintenance logs, phone records, and scene images. If these items are not preserved early, they may be overwritten, deleted, or harder to access. The Influence of Financial Strain on Choices in Personal Injury Settlements often reaches beyond money and weakens proof itself.

Think about how this affects leverage. When liability is clear and damages are documented, insurers face greater risk if the case moves forward. When records are incomplete, they gain room to dispute fault, treatment, or future losses. A rushed file often produces a rushed number. For readers sorting out coverage questions after a collision, health insurance after car accidents often becomes part of the pressure, while car accident settlement limits shape what recovery may look like in practice.

The Influence of Financial Strain on Choices in Personal Injury Settlements also carries a psychological cost. Financial hardship affects sleep, focus, and patience. Family tension rises when one paycheck disappears and childcare, transportation, and co-pays keep stacking up. In those moments, people do not make poor choices because they are careless. They make them because survival feels immediate. That is why legal guidance matters most when money is tight, not after the release is signed.

What should you watch for before accepting an offer? Start with the basics.

- Has your doctor given a clear diagnosis and likely recovery timeline?

- Do you know the full amount of lost wages and missed work opportunities?

- Have future treatment needs been estimated?

- Has key evidence been preserved?

- Do you know whether the insurer is asking for a full release?

Legal decisions look different when the rent is due

The Influence of Financial Strain on Choices in Personal Injury Settlements often shows up in one hard question. Wait for a fuller result, or take a smaller amount to stop the bleeding now? That question is legal, but it is also human. Financial stress affects how people read paperwork, value risk, and respond to pressure from adjusters who want a fast close.

By 2026, consumer protection attention around medical debt has helped some families avoid immediate credit damage, but the pressure has not disappeared. Medical debt does not always show up on credit reports right away, and larger unpaid balances usually need to age before reporting thresholds are met. Still, delayed credit harm does not solve the grocery bill, the utility notice, or the need for gas to reach appointments. The Influence of Financial Strain on Choices in Personal Injury Settlements remains intense because day-to-day life keeps moving even while a claim is pending.

Some injured people have options short of taking the first offer. Medical providers sometimes agree to treatment on a lien basis, meaning payment comes from a future recovery. Some creditors offer hardship plans. In some cases, litigation funding enters the picture, though fees and terms deserve close review. The point is not that every alternative fits every case. The point is that the first check is rarely the only path. The Influence of Financial Strain on Choices in Personal Injury Settlements weakens when a person sees more than one option.

This is also where the right lawyer changes the tone of the case. A skilled attorney looks at liability, damages, insurance layers, filing deadlines, and proof. The lawyer also acts as a buffer between a struggling household and an insurer pressing for a quick signature. If your accident involved rideshare issues, for example, questions similar to whether you need an Uber car accident lawyer affect strategy early. If you are still searching for representation, guidance on finding the right accident lawyer helps frame the decision.

One final point matters. Personal injury settlements are supposed to replace loss, not create a windfall. When financial strain distorts the decision process, the result is often underpayment for future care, reduced earning ability, and the hidden personal cost of living with pain on a smaller budget. The Influence of Financial Strain on Choices in Personal Injury Settlements is powerful because the wrong choice often feels reasonable in the moment. That is why slowing down, documenting losses, and protecting evidence often lead to better legal decisions.

What You Should Do Before You Say Yes to a Fast Settlement

The Influence of Financial Strain on Choices in Personal Injury Settlements does not mean every early offer is unfair. Some cases resolve quickly for sound reasons. Liability may be clear. Treatment may be complete. Future care may be minimal. But you should know why an offer is enough before you accept it. You need numbers, records, and a realistic view of what your injury has changed.

Start by gathering every loss tied to the event. Include emergency care, follow-up visits, prescriptions, therapy, travel costs, work absences, and any job restrictions. Then ask whether your symptoms are stable. If not, the case value may still be moving. The Influence of Financial Strain on Choices in Personal Injury Settlements eases when the claim is built on records instead of fear.

Ask hard questions during settlement negotiations. Does the offer account for future treatment? Does it cover lost income if your work hours stay reduced? Does the release end every claim related to the accident? If the answer is unclear, pause. Quick money solves one problem and sometimes creates three more.

There is also a courtroom angle. If negotiations fail, the strength of your file matters under the rules of evidence. Judges do not rely on assumptions. They rely on admissible proof. That means preserving documents, obtaining statements, and tracking medical updates in an organized way. The Influence of Financial Strain on Choices in Personal Injury Settlements weakens when the case is prepared as if it may need to stand in court.

The takeaway is practical. If you are under financial hardship, address the pressure directly instead of letting it quietly decide the claim. Ask providers about payment arrangements. Review insurance coverage. Consult counsel before signing anything. Speak with family about the trade-off between short-term relief and long-term stability. Then make the choice with full information, not panic. If this issue has touched your life, share your experience or send this article to someone facing the same pressure.

En bref

The Influence of Financial Strain on Choices in Personal Injury Settlements explains why many injured people accept less than they need when daily costs rise faster than recovery. Early offers often arrive before doctors know the full extent of the injury and before evidence is fully preserved.

Financial strain, financial stress, and economic pressure do more than create anxiety. They shape legal decisions, weaken patience, and narrow the focus to immediate bills instead of future losses. The stronger move is often to document everything, protect evidence, review alternatives, and seek advice before agreeing to final compensation.

Why do insurance companies make early settlement offers?

Early offers help insurers close claims before the full medical picture and long-term losses are clear. When claimants accept too soon, the total payout is often lower than what a fully developed case might support.

What happens if I sign a release and my injury gets worse later?

In most cases, signing a release ends the claim. If new treatment, complications, or lost income appear later, you often cannot return for more compensation tied to the same injury.

Does medical debt hurt credit right away?

Not always. By 2026, many medical debts do not appear on credit reports immediately, and reporting often depends on age and amount. Even so, unpaid medical bills still create heavy financial stress during recovery.

What can I do if I cannot afford treatment while my case is pending?

Some providers offer lien-based treatment or payment plans, and some creditors offer hardship arrangements. Review every option carefully with a lawyer so short-term relief does not create bigger costs later.